BKS News

Jersey – a Positive Impact→

Christmas Wishes→

Ten Year Anniversay→

BKS shortlisted for Family Office of the year→

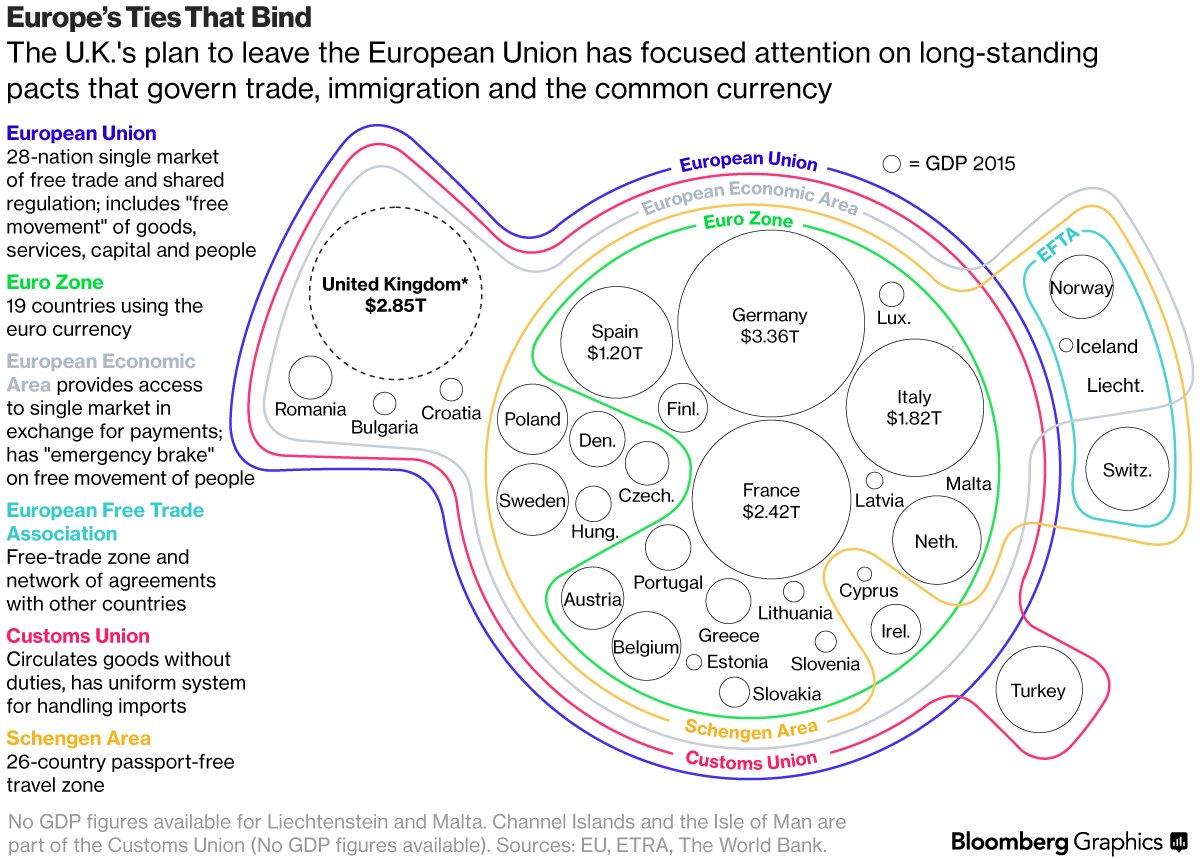

European Ties – Brexit→

Disclosure of Beneficial Ownership→

Season Greetings and Office Hours→

Jersey Relay Marathon→

Contribution to Age Concern Jersey→

HMRC publishes guidance to Non-UK residents on Capital Gains tax→

Season’s Greetings→

New Joiners→